A critique of the social democratic argument that increasing taxation on LNG companies is part of a viable strategy for a better society.

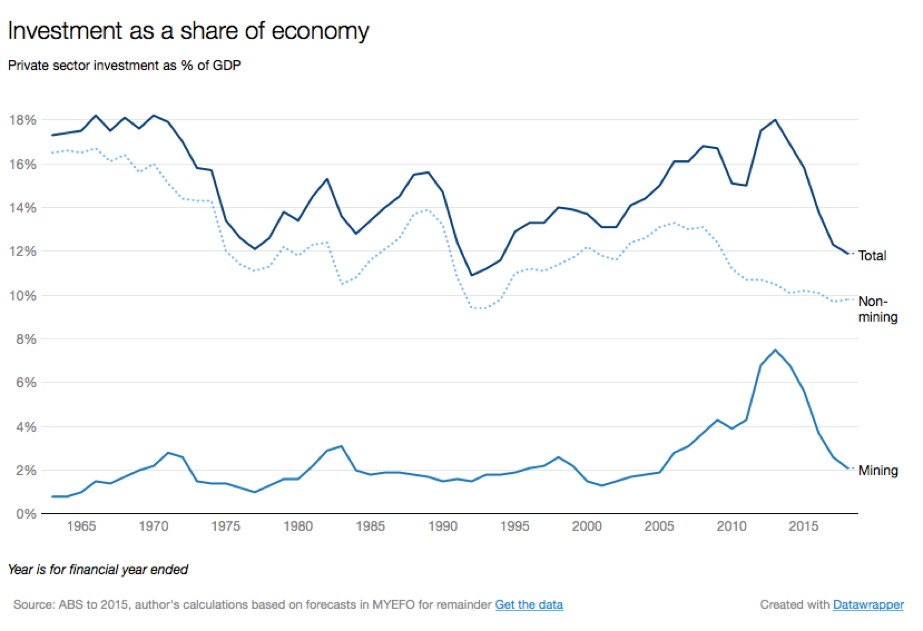

The issue of tax has become a clear line of debate for mainstream politics in Australia. The general malaise of global capitalism expresses itself in Australia in slowing growth and rising state debt. As 2016 came to an end, we have saw the first negative quarter of GDP growth in years, stagnating wage and profit growth and rising state debt and deficits (and Australia’s AAA rating is still vulnerable)(AAP 2016) . The decline in mining construction investment has not been effectively offset by resource exports, services exports or the inner-city off-the-plan unit investment boom. Apart from the drop in investment we saw during the early 1990s recession, investment as a percentage of GDP is currently at its lowest point in 50 years.

(Potter 2017)

(Potter 2017)

Thus, the Turnbull–Morrison government is desperate to stimulate capital accumulation and manage the debt. Their current strategy is as follows: cut company tax in an attempt to increase the supply of capital and thus hopefully increase investment and cut forms of social spending so more spending can be refocused on infrastructure investment (Morrison 2016)[i]. The latter itself functions as a way of both increasing productivity and is meant to be stimulative in its own right. This is a slightly modified version of the previous Abbot–Hockey plan which aimed to more aggressively attack social spending and pursue state-level privatisations to generate funds for infrastructure. In many ways, this approach is one that is being argued for globally. Unorthodox monetary policy—that is, lowering interest rates—has proven to have a less than impressive impact and is in itself facilitating the generation of increasing amounts of debt and risk globally.

The current strategy then is to take the tax burden off the richest and push much of the costs and the work of looking after society (what we can call reproductive labour)(see Katsarova 2015) back onto the wages of the vast majority. This means a greater burden is placed on reproductive labour in the home and thus, onto the shoulders of (mainly) women. Workers must pay more and do more to keep society functioning sufficiently well in a way that allows capital to generate sufficient profits.

It is no surprise then that many people who don’t want this to be the future and in fact would like a society of dignity and justice mount a counter-argument: capital (often framed as ‘the rich’ or ‘multinational corporations’) should be paying more tax and we should be spending more on social services. This is often coupled with an argument that increased spending and increased wages will relaunch capital accumulation by increasing effective demand. Tax policy then will save the economy and produce a better life (which is pretty much a negative inverse image of the claims that the Right make about cutting taxation).

A prime example of this is the argument made by the International Transport Workers Federation (ITF) that LNG-producing companies are avoiding an appropriate level of taxation. This argument is being made in the context of a Federal Government review into the Petroleum Resource Rent Tax. The very tax that the ITF, as part of the Tax Justice Network, say is failing (Hutchens 2016)

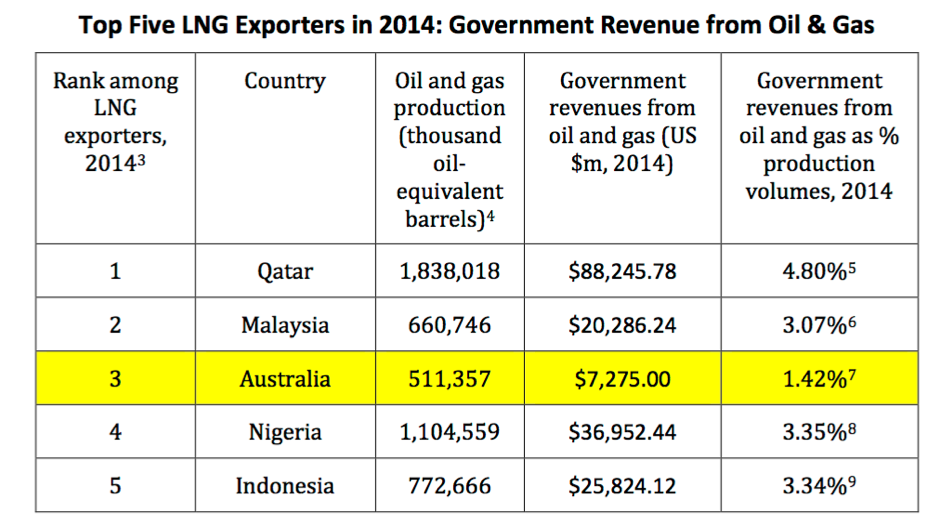

This argument has many convincing elements to it. Compared to other LNG-producing nations, Australia’s tax revenue for this export is low.

(International Transport Workers Federation 2016, 2)

(International Transport Workers Federation 2016, 2)

The ITF argues that the reasons for this are twofold. First, the Petroleum Resource Rent Tax is a tax on profits rather than a royalty:

With the exception of the North West Shelf project area, Australia has no royalty payable on offshore oil and gas production in Commonwealth waters. The PRRT is not a royalty payment but a profit-based tax. While the tax rate is set at 40% it is not forecast to collect any revenues on LNG production for decades. Effectively this means that Australia’s offshore oil and gas is being given away for free

(International Transport Workers Federation 2016, 2).

Second, this is exploited by companies who structure their operations in a way that minimises the size of their taxable profits.

The ITF focuses on Chevron—the owner of the largest shares of investment in the Gorgon and Wheatstone LNG projects. They demonstrate that Chevron has a ridiculously complex set of shelf companies based through tax havens, which allow them to avoid paying the tax. It achieves this by using the shelf companies to loan money to itself at above market rate, thus, making their core business units appear unprofitable (2015a).

The ITF continue that if this situation changed, the revenue could be used to fund social services. Paddy Crumlin, President of the ITWF (and National Secretary of the MUA), argues that ‘If Chevron and its partners can be forced to pay their fair share of tax revenues on these massive LNG projects, it has the potential to increase funding for schools, hospitals and other essential public services’(International Transport Workers Federation 2015a, 15). Thus, the argument of the Turnbull–Morrison government that we must all face the burden of increased cuts and user-pay costs is defeated by showing all we need to do is tax the richest of the richest appropriately.

Well this sounds good, doesn’t it? Leaving aside the question about what is the relationship of increasing state spending to creating a viable and desirable postcapitalist society (spoiler alert: the relationship between the two may be less than what the Left has assumed), what this argument ignores is the perilous state of the global economy. It accepts optimistic projections of future exports of LNG, which are based on very optimistic predictions for the global economy—both of which are unlikely to materialise. The ITF’s (2015b) argument is premised on the LNG market entering a boom period in the years ahead. How likely is this boom?

Now none of us know what will happen. The future is, after all, unwritten. Will Trump’s plan to increase industrial investment in the USA through infrastructure spending, aggressive cuts to taxes and regulation and increasing tariffs against imports, while torpedoing global free trade agreements increase investment and growth or generate further instabilities and risks—or both?

What we can say is the projections about Australia’s future LNG exports have contained more than their fair share of hot air. Take Queensland Treasury’s predictions. Over the last few years Queensland Treasury has been forecasting an LNG export boom that will save the State. However, with each year passing, the projected growth is downgraded. The 2013–14 Queensland Budget stated that, ‘Specifically, the ramp up in LNG production will drive growth in overseas exports by 23¼% in 2015–16 which, combined with a stronger domestic sector, will boost economic growth to 6% in that year’ (Queensland Government 2013, 27). The 2014–15 Queensland Budget stated:

The ramp up in LNG production is expected to underpin a surge in overseas exports of 22½% in 2015–16 which, combined with an improved domestic sector, is forecast to boost economic growth to an 11-year high of 6%

(Queensland Government 2014, 25).

However, by 2015 these expectations had been both deferred and downgraded:

Reflecting this, following two years of subdued outcomes, growth in Queensland gross state product (GSP) is forecast to strengthen to 4½% in both 2015–16 and 2016–17, driven by the surge in liquefied natural gas (LNG) exports

(Queensland Government 2015, 22).

More devastatingly, the Australian Bureau of Statistics showed that in reality, GSP for Queensland in 2015–16 was only 2% (Australian Bureau of Statistics 2016).

Chevron itself is having a worse and worse time of it. Its 2015 annual report states:

Our full-year 2015 net income was $4.6 billion, down from $19.2 billion in 2014. Our sales and other operating revenue were $129.9 billion, down from $200.5 billion in 2014. We achieved a 2.5 percent return on capital employed versus the 10.9 percent achieved in 2014

(Chevron 2015, 2).

Of course, this could be bullshit; Chevron could be hiding its profits. It could be manufacturing an illusionary level of loss. Nevertheless, it is still the narrative that Chevron is communicating to its investors and creditors.

However, most damning are the arguments made by the LNG industry itself—what they say is demand outstripping supply. It is a clear case of over-accumulation where the investment in LNG production has vastly increased supply and thus, prices are falling, worsened by pricing deals that link LNG prices to oil. As the gas industry consultants Gas Strategy write, increased levels of LNG production means a ‘surge of 22 mt of additional supply into a global market where demand in the two largest markets, Japan and Korea, which accounted for nearly 50% of global imports in 2015, has been falling’. The report written at the start of 2016, noted that LNG gas prices had plummeted: ‘LNG and natural gas prices in the main markets will start the year between 35% and 45% lower than they were at the beginning of 2015’(2016, 2).

The International Gas Union, a gas industry association, is equally worried. ‘With gas price benchmarks around the world facing pressure, supply–demand fundamentals will continue to adjust … Given current LNG price levels, suppliers will face lower revenue generation than in the recent past’ (2016, 56). They are worried about a host of issues related to over-accumulation, including if new projects with be viable or not.

This isn’t a simple question of too much supply, sending signals to the market to shift and find equilibrium. This is a question of a deep structural malfunction within capitalism. Capital has developed to such a level that it is undermining its ability to raise sufficient profits. This plays out both on the level of individual firms and on the level of the world market.

The real existing capitalist mode of production that exists in real existing capitalist societies can break down or malfunction in many different ways. The capitalist mode of production consists of multiple separate and competing firms that are all focused on realising profit—turning money into more money. They exist like a serious of interlocking and expanding ‘spirals’ with each individual firm dependent on a vast web of other firms (Luxemburg 2003, 7). The basic form of the capitalist mode of production, the commodity, has within itself the potential for crisis because a firm can take its products to market and fail to sell them (Marx 1969, 508). There is also a deep structural tendency towards crisis that grows out of capitalism’s very dynamism and success.

While there are multiple ways that individual firms can turn money into more money, the core of capitalism is the workplace where workers are pushed to work in a way where what they contribute to the production of goods and services is then sold realising greater volumes of money than what they received in wages. Thus, they create ‘surplus value’: the ultimate wellspring of profit and of capital itself (Marx 1990). This is an exploitative and antagonistic relationship that lies at the heart of capital. The historical unfolding of this antagonism takes shape as the constant compulsion to push more and more from us and as our attempts to resist this imposition; to shorten the burden of work and increase the space for a quality of life. An outcome of this antagonism has been the increasing deployment of technology by capital.[ii] Deploying technology is about increasing our subordination to capital: to increase the productivity of labour, to increase the ratio of surplus-value; to increase the difference between wages and the value of output and to produce and sell commodities cheaper than the market price and thus, increase profits. Competition between firms means that each advance in technology soon sets a new benchmark that all companies must meet or go under. In this way, our struggles inside-against-and-beyond capitalism work as the ‘motor-force’ that drive it (Holloway 2002, 161).

This creates a general tendency in capitalism to increase the ratio of capital spent on technology in relation to that spent on wages and to an increase in the size of individual capitalist firms. However, paradoxically, as capital grows larger and more productive and the mass of profits increase, the ratio of profit to investment decreases (Marx 1991). Profits begin to shrink relative to the size of investment even as they grow in mass. Since the entire purpose of a capitalist firm is the endless accumulation of more capital, this functions as a barrier to growth and the seeds of crisis. Firms that are growing in size and productivity produce more than can be sold at a level to satisfactorily reward investment.

Credit and finance works to both delay and intensify this crisis:

If the credit system appears as the principle lever of over-production and excessive speculation in commerce, this is simply because the reproduction process, which is elastic in nature, is now forced to its most extreme limit…

(Marx 1991, 572)

Debt works to increase spending for workers and capital. Financial speculation functions as an alternative source of profits. But at some point there exists the possibility that as investment shrinks in relation to soaring debt and speculation, the whole thing falls apart. As an investment contract, debts can’t be met, sales collapse, the value of financial assets falls, unemployment rises and so on.[iii] Thus, capital fails in its ability to successfully exploit labour and realise that exploitation in continued capital accumulation. Crisis is the failure of a relationship of domination (Holloway 2016).

Crises function as a way of cleaning out the system. The collapse in prices and the closure of businesses, the immiseration of workers and the crushing of living standards, opens the way for the next wave of investment and the next boom. ‘And so we go around the whole circle once again’(Marx 1991, 364). However, the very misery caused by the crisis also threatens the stability of the system. There is always the potential that we will overthrow the whole shitty business. The level of repression necessary to hold us down can jam the functioning of the normal social order and different capitalist nation-states competing for slices of a shrinking market pie can end up at each other’s throats. Indeed, the ‘solution’ to the Great Depression which laid the basis for the Golden Age of Capitalism in the 1950s and 1960s was the destruction of the Second World War; destruction of capital and destruction of life.

This is where we are at now. The response of capital to the crisis of the 1970s was a flight to either the global South, into new technological industries and services, or into finance (Midnight Notes Collective 1992, Midnight Notes Collective and Friends 2009). The vast growth in finance allowed the booms of the 1990s and 2000s. In the face of a growing crisis and malfunctions, central banks pumped in cheap money to keep everything going and the industrialisation of China and South East Asia powered capital accumulation. Debt, at the level of the household, state and firm, kept consumption functioning while wages stagnated. Financial speculation compensated for the tendency for the rate of profit to decline. In a world saturated with capital, more profits were directed away from productive investment and into finance. Finance had become ‘co-substantial’ with the entirety of the economy (Marazzi 2011). This all exploded in 2007–8. As the inflated values of financial assets collapsed, the over-accumulation of capital was exposed and the whole system could only be maintained through bail-outs—huge transfers of wealth from the state to finance capital and debt from capital to the state. Unorthodox monetary policy (basically central banks printing money and promising to buy billions after billions of finance assets) kept the wheels turning and for countries like Australia, stimulus in China worked to defer the crisis and allowed the continuation of mining investment.

This is a ‘holding pattern’ where the intervention of states has held off the crisis hitting rock bottom, but also prevented it from cleaning out the system and laying the basis for the next round of accumulation (Endnotes 2013). However, this has led to even more debt and thus, accumulated risk (McKinsey Global Institute 2015). The capacity of stimulus in China has hit limits of declining investment and rising working class struggle (Hung 2015, Kumar 2016). Both the IMF ( 2016) and OECD (2016) have a grim outlook for global growth.

The oversupply of LNG is then, just one manifestation of this historical dynamic and systemic logic. During the boom, especially during the rising industrialisation of China, the values of resource commodities skyrocketed and capital flooded into mining construction. This has led to the current situation whereby the capacity of these LNG mining projects outstrips effective demand and faces generally much lower prices (with upswings now and again).

What does this all mean? We should keep our hubris in check and remember the old joke that Marxists have correctly predicted 13 of the last two economic crises. No-one knows what will happen. However, there is a good argument based on the empirical state of the LNG industry and, I think, a convincing theory of the dynamics of capital, that this LNG boom is less likely than likely. But to quote CLR James, ‘As has been said on so many occasions: we shall see’(2013, 74).

So what? Why do we care about the fortunes of the rich? Why should we be concerned about the profits of MNCs? Well if your strategy, like that of the ITF, is that you can realise considerable tax revenue through the success of profitable companies, then if these companies aren’t doing well your strategy becomes unhinged. A more difficult point to consider is what impact increased taxation might have on a company facing an increasingly shaky future. All firms are disciplined by the ‘coercive laws of competition’ (Marx 1990, 433) . They must return an acceptable level of profit in relation to the costs of investment or capital will flee from them and the costs of borrowing will increase. Capital flees from unprofitable investments. Now many will point out that resource production is hard to run from since resources are in the ground and the fixed capital investment is normally sizable and costly. However, in a world of unsteady growth and the over-accumulation of resource commodities, we should be aware that it wouldn’t take much for investors to run elsewhere, for lending to become more expensive and for companies like Chevron to think that perhaps lower levels of production or mothballing a site is more appealing than pouring away capital.

More importantly, this misreading of the state of the LNG industry by the ITF is evidence of their misreading of global capitalism and how much their world view has internalised the deeply erroneous mainstream neoclassical economics understandings. It is a strategy that obfuscates one of the key fundamentals of our life: we live in a storm. A storm composed of economic crisis, the breakdown of political structures and increasingly reactionary and violent politics (Contributions by the Sixth Commission of the EZLN 2016, 182-83). There is no nice normal ahead where capital can keep growing and we can take an increasing slice of the pie to make our lives nicer. Who knows how this will end? But if we want a world where we can live good lives, then we need an approach that is as radical as reality: both anticapitalist and premised on the acceptance of the violent fragility of the current state of things.

Second, the next problem is that of democracy and the state. The argument made by the ITF is that we can we can use the state to increase taxation and then this revenue will be spent making our lives better. How is this to be done? The ITF strategy seems to be one of pressuring the state to do so. Even in the context of the Federal revenue, how likely is it that the government will both increase taxation and then use these funds to increase spending on social welfare?

One suspects that the hope of the ITF is that the demand for increased LNG taxation would both aid an ALP victory and that an ALP victory would help them realise their plans. This overestimates the power and importance of nation-states in the world market. Individual states are embedded in the broader flows of capital (Holloway 1996, 2002). States must act in ways that ensure and facilitate the generation of profits or they will be undermined or deserted by capital. We should of course remember the incidence of the Minerals Resource Rent Tax, where the attempt by an ALP government to increase mining royalties was quickly defeated by a very mild opposition from multiple sections of capital. The history of the ALP’s continual capitulation to capital is a story not just of weak and sell-out politicians. As Frank Hardy (1975) argued in Power Without Glory, the ALP is not just home to the criminal John Wests and the cynical and corrupt Ted Thurgoods of the world. Its subservience to managing the state means it is a machine for destroying the honest and committed Frank Ashtons too.

There are two levels of explanation for the constant failure of parliamentary parties to realise our hopes. On one level, we live in a deeply unequal society. Despite the formal equality of all citizens and the capacity to vote, the significant difference in levels of wealth and in power to command capital means individual capitalists have vast influence. However, the state itself is still subordinate to the functioning of the capitalist mode of production, even if it were free from the influence of the Murdochs and Forrestors and their like. The state’s main task is ensuring both the reproduction of the capitalist mode of production and the reproduction of a society which allows for the smooth functioning of the capitalist mode of production. If you want to keep society running, you become compelled to stoke the fires of capital accumulation—lest you be beset by declining growth and rising unemployment.

What does this suggest? That we should do all to ensure capital accumulation? Rather it means we need an approach that aims beyond capitalism. Reality compels us to be increasingly radical. The fantasy of ‘capitalism with a human face’ remains just that (Žižek 2000). If our plans to create a society worth living in hinge on the successes of capital accumulation continuing, then the reality of the latter will constantly force us to abandon the former and the latter will probably malfunction anyway. Rather than spending our time (and members’ money) lobbying upwards to the state, it is far better to look around us to the terrain of our own lives and see what is going on there. What kinds of forms of solidarity exist? What struggles exist? Is there a way to widen this space, to increase our cooperation with each other and our opposition to capitalist society? Sometimes this does not look like much, but this is where our hope lies. A more useful thing for unions to do, rather than write position papers for politicians and the political class or to campaign for the ALP or even the Greens, is to provide resources, funds and equipment to the members themselves to do as they wish.

It is worth remembering what is driving the dynamics of the capitalist mode of production is the attempt by capital to subordinate us further and further. Crisis, then, is a breakdown in the social relations of capital; a breakdown in the enforcement of subordination. Thus, we can say with Holloway, ‘We Are the Crisis Of Capitalism and Proud of It’(2016, 1).

This blog post arises out of a request from a friend and comrade to provide my thoughts on this issue. I am happy to take such proletarian commissions. Also Ali edited this post –saving me a great deal of embarrassment and presumably the readers a headache. Thank you so much.

[i] A particularly vicious manifestation of this has been the attempt to shake-down people for real or alleged welfare over-payments using a combination of data matching, bureaucratic stone-walling and debt collection companies. The government aims to squeeze out $4 billion in four years (Dempster 2017).

[ii] ‘But machinery does not just act as a superior competitor to the worker, always on the point of making him superfluous. It is a power inimical to him, and capital proclaims this fact loudly and deliberately, as well as making use of it. It is the most powerful weapon for suppressing strikes, those periodic revolts of the working class against the autocracy of capital. According to Gaskell, the steam-engine was from the very first an antagonist of ‘human power’, an antagonist that enabled the capitalist to tread underfoot the growing demands of the workers, which threatened to drive the infant factory system into crisis. It would be possible to write a whole history of the inventions made since 1830 for the sole purpose of providing capital with weapons against working-class revolt’ (Marx 1990, 562-63).

[iii] I want this distance myself here from a robotic or overly deterministic interpretation of the tendency of the rate of profit to fall, acknowledge the complexities and contradictions and reject the idea this all leads to a final crisis. While there are certainly problems with arguments that profit is becoming rent (see Fumagalli and Mezzadra 2010), we need to take into account the way that capital appears to be fleeing investment in both means of production and labour, and is extorting profits via ownership of key algorithms and the outsourcing of production to the end-point user. This is typified in the rise of the Uber/Sharing economy.

Comments